")

Fintech software development compliance intake questions aren’t optional at SynthWeb, they’re what the first 20 minutes of a discovery call are built around, whenever the founder on the call is building in fintech or insurtech. We are not asking what you want to build; we already have that from the brief. Instead, we’re asking 12 specific questions whose answers change the architecture, the timeline, the team composition, and the price of the build. These 12 questions come directly from the Torus cyber insurance platform engagement, which taught us that compliance constraints discovered in week six cost three times more to accommodate than compliance constraints discovered in week one.

The questions fall into three groups.

Group 1: Fintech Software Development Compliance Intake Questions — Regulatory Landscape (Q1–Q4)

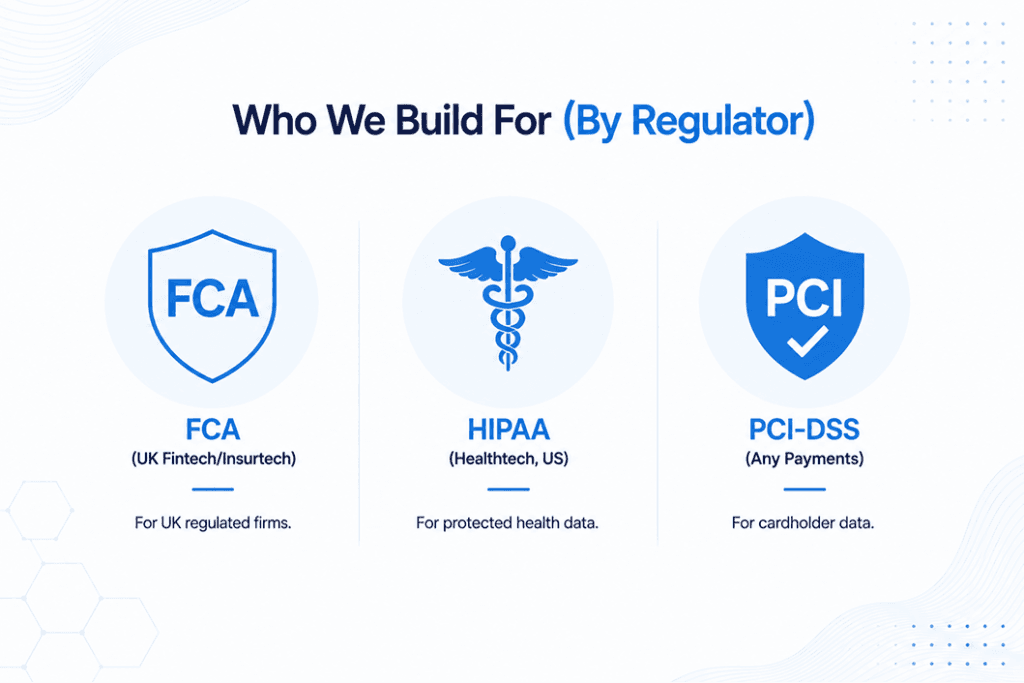

Q1: Which regulator applies?

FCA for UK fintech and insurtech. HIPAA for US healthtech involving protected health information. PCI-DSS for any product handling card data. GDPR for any product handling EU personal data (which is almost all of them). Multiple regulators can apply simultaneously — a UK fintech handling US payments touching EU users has all four. The answer to this question determines the compliance layer architecture.

Q2: Are you in regulatory sandbox or applying?

Both the FCA and the EMA have sandbox programmes that allow limited live operation before full authorisation. Building in sandbox mode changes the data residency requirements, the reporting obligations, and the audit timeline. If you are applying for authorisation post-build, the application needs engineering evidence — audit logs, security reports, access control documentation. This adds two to four weeks to the build.

Q3: How is personal data classified?

Tier 1 (financial data, health data, biometric data): maximum encryption, strict access logging, data minimisation by design. Tier 2 (standard personal data, business contact data): GDPR-standard handling. The classification determines the database architecture, the access control model, and the backup retention policy.

Q4: Does the product handle payments, and at what level?

PCI-DSS compliance requirements depend on how card data flows through the system. A product that uses Stripe Elements and never sees raw card numbers (SAQ A) has very different requirements from a product that processes card data on its own servers (SAQ D). SynthWeb always recommends the Stripe Elements path — it moves PCI scope to Stripe rather than the client product.

Group 2: Data and architecture (Q5–Q8)

Q5: Do you have geographic data residency requirements?

UK data staying in UK regions, EU data staying in EU regions, US data staying in US regions. Multi-region architecture adds 20 percent to the infrastructure setup and ongoing cost. If you are not sure whether you have residency requirements, the answer is probably yes — ask your legal advisor before the scoping call.

Q6: What are your retention and deletion obligations?

Financial records in the UK: six years retention. Health records: varies by type and jurisdiction. GDPR right to erasure: personal data must be deletable on request without breaking the product. The deletion architecture has to be designed from day one — retrofitting a deletion pipeline into a system that was not built for it is a two-to-four sprint project.

Q7: Is audit logging required?

For FCA-adjacent products, audit logging is effectively mandatory. For products with enterprise B2B customers, audit logging is a sales requirement — procurement teams ask for it. SynthWeb builds audit logging as a standard feature on all regulated-industry builds, because it’s one of the fintech software development compliance intake questions that pays for itself fastest. The Torus audit log added 15 percent to the engineering cost and closed three of their first 20 enterprise customers.

Q8: Do any third-party integrations handle regulated data?

If your product sends user data to a third-party analytics tool, CRM, or communication platform, each integration requires a Data Processing Agreement and a security assessment. This is a legal task, but it needs to be completed before the integration is built, not after.

Group 3: Operations and team (Q9–Q12)

Q9: Do you have a compliance officer or legal advisor?

If yes, SynthWeb works directly with them on the technical controls. If no, we recommend engaging one before starting the build. Legal gaps discovered mid-build are expensive.

Q10: Do you have existing compliance documentation?

Policies, risk assessments, a data map. If yes, we work from these. If no, we flag the gap — compliance documentation is the legal team’s scope, not engineering’s.

Q11: What is your planned certification timeline?

SOC 2 Type II, ISO 27001, FCA authorisation — each has a timeline that the engineering build needs to support. If certification is planned for six months post-launch, the build needs to produce the evidence artefacts from day one.

Q12: Have you had a prior security incident?

An honest answer here shapes the security posture of the build. Prior incidents often indicate systemic gaps that need addressing before building new features on top of them.

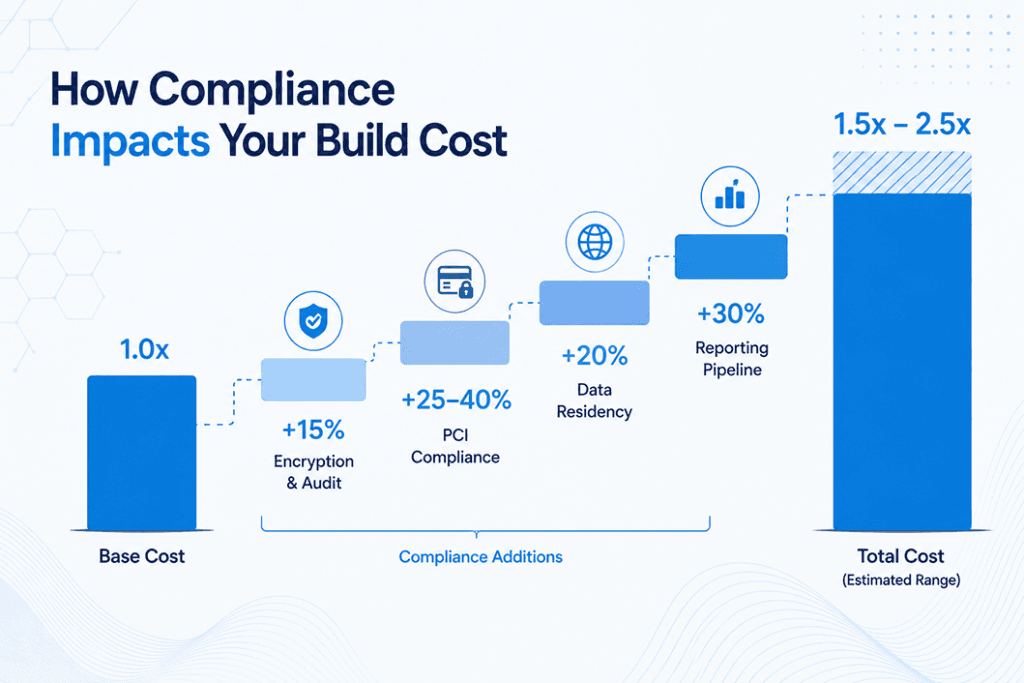

The cost multiplier

Standard MVP Sprint ($28,000–$45,000) assumes no compliance. Add-ons: encryption at rest and audit logging +15 percent, PCI-DSS payment handling +25 to 40 percent, multi-region data residency +20 percent, regulatory reporting pipeline +30 percent. A compliance-heavy fintech build is typically 1.5 to 2.5 times the base rate. Retrofitting compliance into a non-compliant codebase is 3 to 5 times the cost of building it right the first time. This is the real cost of skipping fintech software development compliance intake questions at the start; you pay for the same work twice, once to build it and again to rebuild it correctly

FAQ : Fintech Software Development Compliance Intake Questions

Can SynthWeb handle PCI-DSS?

Yes, via Stripe tokenisation. We do not handle raw card data.

Do you work with our legal team?

Yes. The Torus engagement involved direct coordination with the client’s compliance advisor throughout the build.

What if we do not know the answers to these questions yet?

Common. The first two to three discovery calls often involve helping the founder understand which regulations apply. We work through this together before quoting.

Also Read:

SOC 2 Readiness Startup Series A: 8 Critical Security Checks Investors Always Demand

")